When most people think about selling their home, they automatically picture spring the yard is green, the flowers are out, and everyone seems to be in house-hunting mode.

But here’s the truth: spring isn’t always the smartest time to sell.

In fact, selling your house this winter may actually give you a major advantage especially if you’re trying to stand out and make a confident financial move.

Let’s break down why winter might be the opportunity most homeowners overlook.

Winter Is When Your House Finally Stands Out

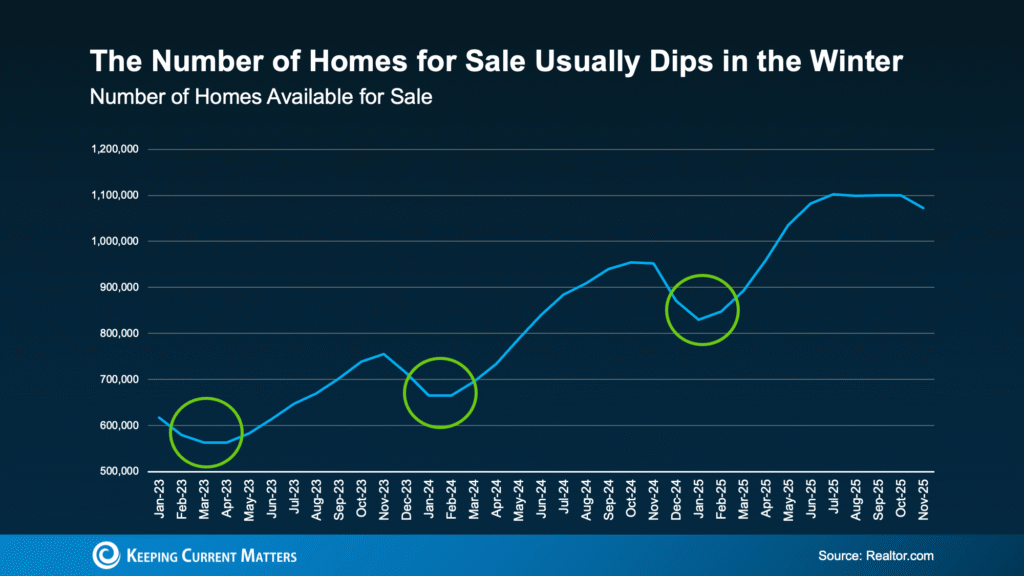

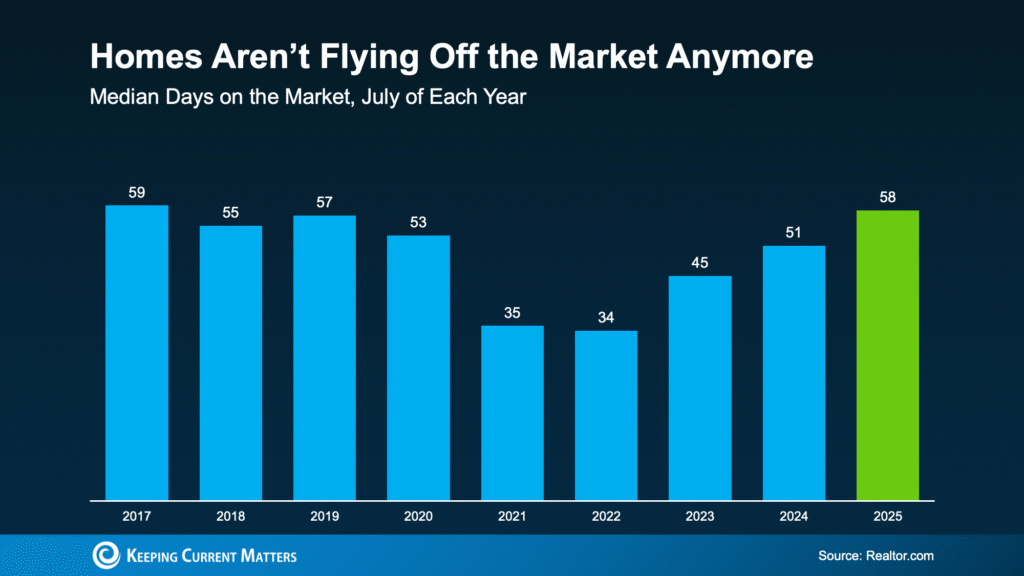

Every year almost without fail the number of homes for sale drops as winter approaches. Realtor.com’s data shows the same pattern year after year: inventory dips in the winter, then rises again as spring arrives.

And based on the latest numbers rolling in for 2025, we’re seeing that same trend start again.

Listings are beginning to decrease as we close out the year and if history repeats itself (which it usually does), inventory will drop even further through winter.

Here’s why this matters for you:

Even with more listings than last year, we still aren’t anywhere near a “normal” market.

Compared to 2017–2019 levels, today’s housing supply is still too low.

So when winter inventory dips again, your home has less competition and more visibility.

Think of it like this:

Less competition = More attention on your home.

If you list now before everyone else rushes back into the market in spring you get ahead of the crowd.

Winter Buyers Are More Motivated Buyers

Another big advantage to selling your house this winter?

The buyers who are shopping right now are serious.

They’re not browsing because it’s fun.

They’re looking because they need to move for a job relocation, a lease ending, a life change, or a growing family.

U.S. News puts it this way:

“Buyers who brave the cold usually have a good reason they need to move and can make quick decisions.”

And with fewer homes available in winter, they have fewer options to choose from. If you price and prep your house well, there’s a good chance your home becomes the one that checks their boxes.

Motivated buyers + low inventory = stronger offers and quicker decisions.

Why Not Wait Until Spring? Why This Matters for Buyers Trying To Stretch Their Budget

Most homeowners wait to list until spring because it “feels” like the right time.

But that’s exactly why waiting could hurt you.

Spring brings more buyers – yes.

But it also brings a flood of new listings.

Suddenly, you’re competing with every homeowner who waited all winter.

Winter gives you the opposite experience:

- Less noise

- Less competition

- More motivated buyers

- A cleaner shot at standing out

Bottom Line: Winter Gives Sellers a Quiet Advantage

If you’re thinking about selling, winter may be your best opportunity to:

Stand out in a less crowded market

Attract serious, motivated buyers

Avoid spring competition

Sell with more confidence and clarity

You don’t have to wait for the “busy” season to make a smart move.

Sometimes the quiet seasons work in your favor.

If you want to understand what listing your home this winter could look like or whether it fits your financial goals connect with a trusted real estate agent in your area.

A good agent can help you make sense of the numbers and take your next step with confidence.

{kind=link}